Registering a charitable organisation?

Before applying to register as a charity you should read the following guidance:

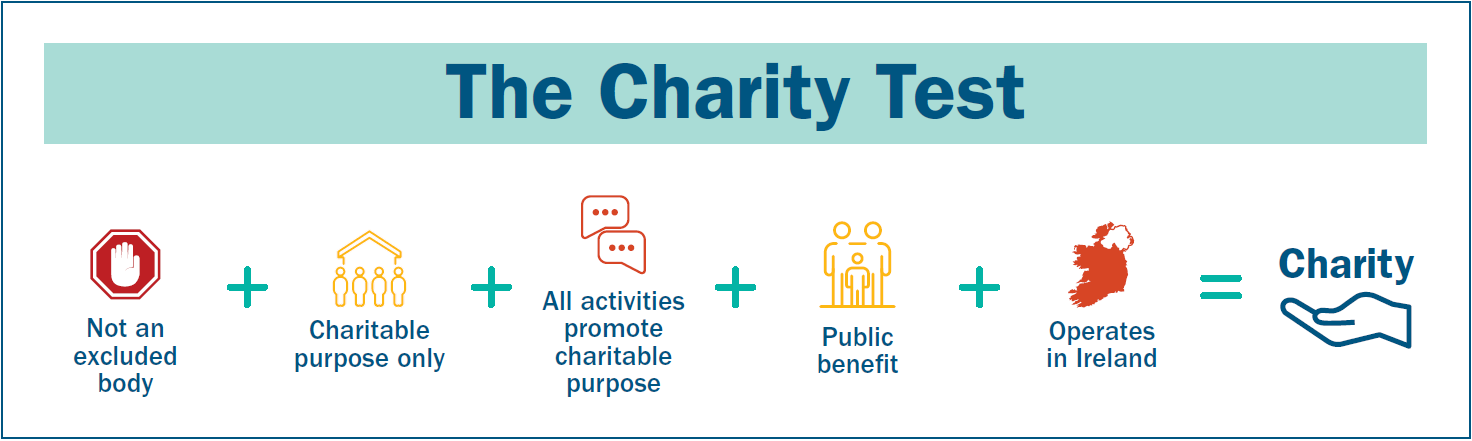

The Charities Act 2009 (the ‘Act’) sets out the requirements that your charitable organisation must meet to be considered a charity. This definition of a charitable organisation can best be illustrated using this simple graphic:

The registration process is legal in nature and is necessarily robust to ensure that Ireland has a vibrant, trusted charity sector that is valued for the public benefit that it provides. In this process your organisation will need to demonstrate it has the ability to advance its charitable purpose or purposes, that it has clear plans in relation to the activities that it intends to carry out to advance that purpose and that it understands which section of the public will benefit and how.

-

Is setting up a charity right for you?

If you are considering registering a charity, before beginning the registration process you should consider if it is the best way to achieve your aim. Ask yourself the following questions:

- Is there an existing charity carrying out the same activities that you could assist as a volunteer or as a charity trustee?

- Do you want to start a charity or do you want to fundraise?

- Do you have the capacity and support to run a charity?

- Will you have the administrative and financial resources to run a charity in the long term?

Have you considered any alternative to a charity?

If you decide that setting up a charity is the right option for you, read on to learn more about the registration process, including some of the documentation, policies and processes required to register and run a charity.

-

Who cannot register as a charity? Excluded organisations

Certain bodies are excluded from registering as charities. If your organisation’s activities match those outlined below you may be an excluded body and we recommend you seek independent advice before proceeding with your application.

- Groups whose sole purpose is to promote an athletic or amateur game or sport are not eligible to register as a charity Sport groups can separately register for a sports body’s tax exemption. For further information, please contact Revenue. There are exceptions to this such as where a charity uses sport as a means to advance its charitable purpose. For example an organisation that is advancing the integration of those who are disadvantaged, and the promotion of their full participation in society uses sport as a means of integrating people with learning disabilities into society.

- Political Parties, or a body that promotes a political party or candidate.

- A body that promotes a political cause, unless the promotion of that cause relates directly to the advancement of the charitable purposes of the body. However, there can be exceptions if the promotion of that cause is ancillary (that is secondary) to the advancement of the charitable purpose(s) of the organisation. For example, an organisation whose main purpose is to provide services to homeless people and has an ancillary purpose to campaign for better services for this group of people may still be considered a charity. For further information see our guidance document: Charities and the promotion of political causes.

- A trade union or a representative body of employers.

- A chamber of commerce.

- A body that promotes purposes that are unlawful, contrary to public morality, contrary to public policy, in support of terrorism or terrorist activities, whether in the State or outside the State, or for the benefit of an organisation, membership of which is unlawful.

-

Who cannot register as a charity? Other reasons

- Failing the Charity Test

An organisation that does not meet each element of the charity test outlined is not a charity under the Act. An organisation that does not meet the charity test cannot be registered as a charity under the Act nor can it refer to itself as a charity.

- Fundraising for an individual

Charities are required to benefit the public or a section of the public. Those fundraising for an individual, or a small number of identified individuals, will not meet the charity test

- Certain 'not-for-profit' organisations

Charities are one type of ‘not-for-profit’ organisation but not all ‘not-for-profit’ organisations are charities under the Act. To be a charity, an organisation must be established for an exclusively charitable purpose or purposes and provide a public benefit. An organisation that has no charitable purpose will not be a charity even if it operates on a non-for-profit basis. An example would be a not-for-profit organisation set up to promote tourism. The promotion of tourism is not a charitable purpose under the Act.

- Organisations that have mixed purposes

Some organisations may have what are described as mixed purposes, where some of the organisation's activities may be charitable and other activities are not. For example an organisation that primarily provides football training to children for a weekly fee and once a week gives training to refugee children for free as a means of promoting social integration. One purpose is excluded, as sport is not considered to be a charitable purpose under the Act, while the other purpose of providing training to promote social inclusion would be considered charitable under the Act. An organisation with mixed purposes would not pass the charity test as its purposes are not exclusively charitable.

- Where the private benefit outweighs the public benefit

Private benefit is a benefit that is gained by an organisation or an individual from the activities of the charity other than as a member of the public or section of the public. Some private benefit is permissible as it is considered necessary in order for the charity to operate and to deliver its service. For example, permitted private benefits are staff salaries and payments made to third-party suppliers of goods and services such as office equipment, rent or accountancy fees are recognised as being ancillary and necessary in some circumstances. However any such payment must also be reasonable.

For a private benefit to be permitted, the charity must demonstrate it is:

- Reasonable in all circumstances

- Ancillary (additional to or providing extra support) to the public benefit to the activities delivering the public benefit

- Necessary for achieving the public benefit

Private benefit will always be assessed to determine whether or not it is permitted. The circumstances of each case will be relevant in assessing the private benefit. The private benefit must not outweigh the public benefit. For further information see our guidance ‘What is public benefit’?

-

Pre-application checklist

Before commencing any activities or submitting an application to register, the following list includes some of the documents you need to read, understand and prepare:

✓

Have you read our Registration guidelines?

✓

Have you read the section on excluded bodies? Are you an excluded body?

✓

Do you know what the organisation structure will be?

✓

Have you drafted your constitution? And do you understand what needs to be included by reading our model constitutions for Companies Limited by Guarantee and Unincorporated Associations?

✓

Do you understand your charitable purpose and have you read What is a charity?

✓

Do you know what activities the charitable organisation carries out and intends to carry out to further its charitable purpose(s)?

✓

Have you read Guidance for charity trustees? Do you have three or more trustees and is the board balanced?

✓

Do you understand conflict of interest and have you read the Guidance for Charity Trustees?

✓

Have you read Safeguarding guidance for charitable organisations working with children?

✓

Have you read Safeguarding guidance for charitable organisations working with vulnerable persons (adults)?

✓

Do you know your objectives to advance your charitable purpose for the next 24 months?

✓

Do you know how the charitable organisation raises and proposes to raise funds?

✓

Do you have details of the number of staff and volunteers?

✓

Do you know the amount of any funds raised by the charitable organisation during the 12 months immediately preceding the application?

✓

Do you have the particulars of all bank and credit union accounts of the charitable organisation?

✓

Do you know the name of each charity trustee and the addresses at which they ordinarily reside?

-

Preparing your application

Once you have gathered all the required documents and information you are ready to submit your application for registration. Time spent preparing the application is well spent as it will reduce the likelihood that your application will be returned to you for more information.

One of the key documents you will need when making your application is your organisation’s constitution. The constitution is the legal document setting out what your organisation is set up to do and how it operates.

The Charities Regulator has a Model Constitution for Companies Limited by Guarantee and a Model Constitution for charitable organisations that are not companies (these are Unincorporated Association such as an Association, society or foundation). The Charities Regulator has designed these model documents to encourage and facilitate improved drafting of the constitution.

There are certain clauses that must be included and if you do not adopt our model constitutions they must be included. We have standard clauses for Companies Limited by Guarantee or for charitable organisations that are not companies.

It is crucial that you submit all required information and documents. Failure to do so will delay your application. The time taken to process your application will depend on a number of factors including the quality of the information provided in the application and the initial documents received by the Charities Regulator; the nature of your application; the overall volume of applications being processed; the type and size of the applicant organisation and your responsiveness to any queries raised.

Creating your Application

The applicant should read and understand the requirements for applying to be registered on the Register of Charities. You can only apply through our online portal, MyAccount. To access MyAccount you need to set up a customer account.

To create a new customer account start by clicking on Create Account link. Once you have entered the required information, a verification email will be sent to the email address you have provided.

The login name, password and email address entered into the customer account will be connected to application form. Keep a record of these very important details. We advise using a general non-personal email address to which more than one appropriate person in your organisation has access for example. info@charity.com.

Once you have set up your account you can create a new application, by clicking on new filing on the left hand side and selecting ‘New Registration Application’.

-

Useful guidance and templates

Guidance

Templates

-

Registration process

The Charities Regulator follows a three-stage process when assessing applications for registration that have been submitted to us.

Stage 1: Document check.

First, applications are checked to make sure they are complete. This means that all sections of the form have been completed and the organisation applying for registration (the applicant) has provided all required documents. Where basic information and/or documents are missing, we will return the application to the applicant.

Stage 2: Assessment by the Charities Regulator.

When we have confirmed that the applicant has provided the necessary documentation, we will assess the application to determine whether it has shown that it meets the legal requirements to be registered as a charity according to the Charities Act 2009. We call this ‘the charity test’.

During this assessment, we will return the application to the applicant if we have any queries or need further information. The purpose of this stage is to assist applicants in providing information to us to address all the elements of the charity test. We recommend applicants address any issues or problems that we identify and return the application with the required information without delay. This will continue the smooth progress of the application.

Stage 3: Decision Making.

Once we have all the required information to allow the application to be assessed against the legal requirements of the Act, the application enters final stage when a decision will be made. An applicant cannot make any changes to an application or withdraw it at this stage. This is in the interest of fairness to all applicants. We have to allocate our resources fairly and evenly. By the time an application reaches this stage, the applicant will have been given sufficient opportunities and information to understand the requirements of the Act.

There are two possible outcomes at the decision making stage: the application is either approved or refused.

Approving an application: If an organisation meets the legal requirements of the Act to be considered a charity, the application will be approved and we will inform the organisation of this decision in writing. The organisation will be issued with a Registered Charity Number and will be added to the public Register of Charities. We will also let the organisation know if its application has been approved subject to the organisation meeting certain conditions. For example, it may be required to file an amended governing document with the Companies Registration Office.

Refusing an application: If an organisation does not meets the legal requirements of the Act to be considered a charity, we will inform the applicant of this decision in writing in a letter called a Notice of Intention to Recommend Refusal of the Application. This letter will explain why the Registration Unit intends to recommend that the application is refused.

Before a final decision is made, the applicant has a right of reply to the notice. This means they have the opportunity to correct any error of law or any misrepresentation of facts that may be contained in the notice. The applicant cannot amend the application or submit additional information that was not submitted to the Charities Regulator during stage two, prior to the decision making stage. An applicant may only submit additional information to support their view that there is an error of law or any misrepresentation of facts in the notice.

Any reply received from an applicant about any error of law or any misrepresentation of facts will be considered before the board of the Charities Regulator makes a final decision on the application.

If an application is refused, the applicant can appeal the decision to the Charity Appeals Tribunal, an independent body established by the Act. Appeals must be submitted not later than 21 days after an applicant receives notification of the decision to refuse, unless the Charity Appeals Tribunal extends the period for appealing the decision.